003 Margin Notes: Beyond Launch

Building the next space economy

Hi Everyone 👋

I recently attended Space Walk III, an event hosted at Space Center Houston to showcase startups across the space and aerospace ecosystems. Given the recent SpaceX IPO news, I expected more conversations about traditional space companies such as rockets or launch systems.

Instead, many of the companies were focused on logistics, construction, energy, communications, biotech, and the systems needed to operate in remote or extreme environments. If “space” had been removed from the company descriptions, many would have looked similar to those we interact with here on Earth.

For most of the space industry’s history, the rocket has been the defining symbol. Standing in the lobby at NASA, we were surrounded by images of rockets, astronauts, and missions beyond Earth. Rockets are the visual defining exploration, ambition, and technological progress.

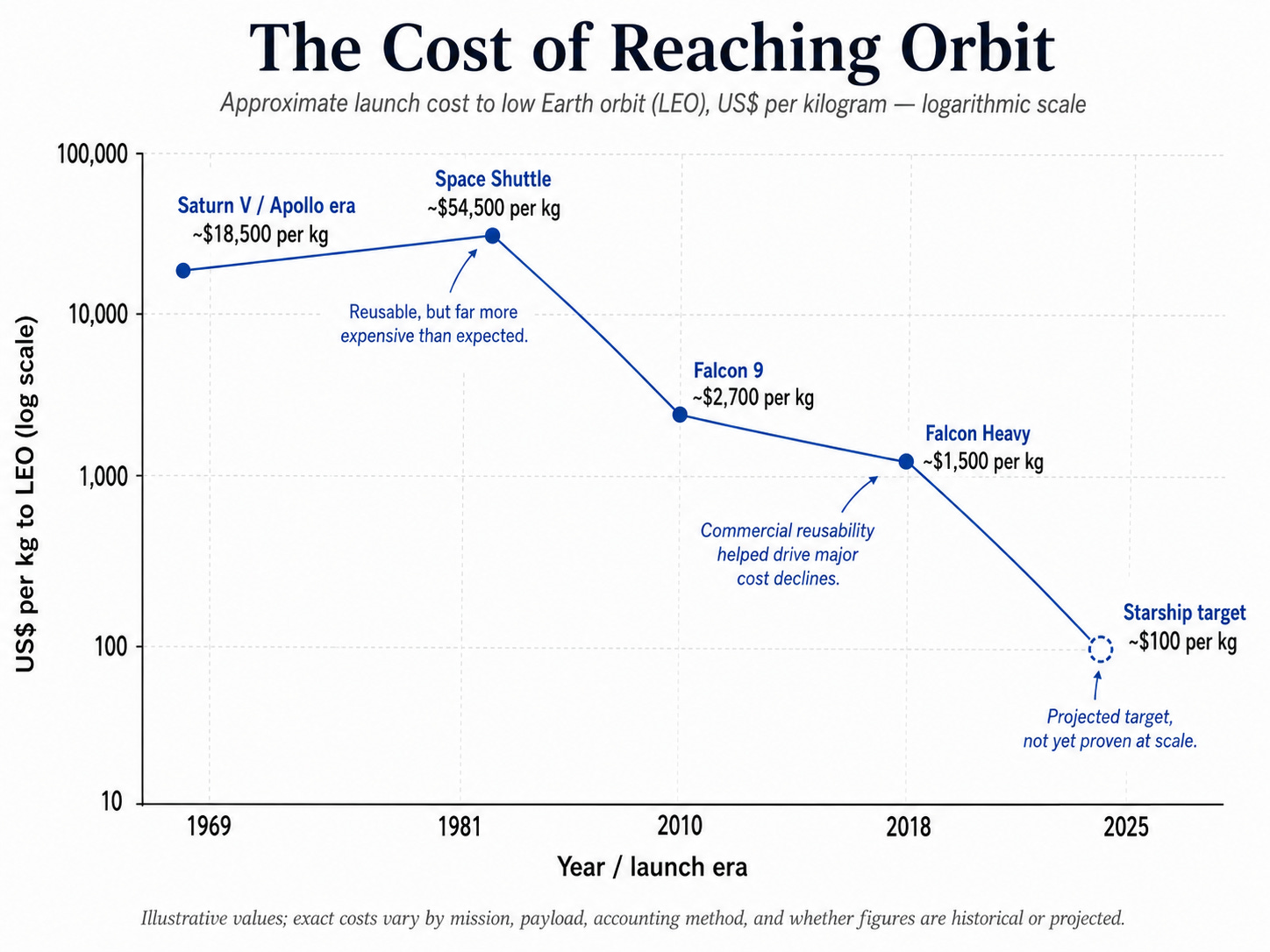

But as launch costs decline and private companies become more active, the investment landscape is shifting. The first phase of the commercial space economy was about access. Can we get there? The next phase may be about infrastructure. What do we need once we arrive?

We wrote about space in November 2022 as a potential investment frontier. Our thesis at the time was that declining launch costs were opening the market to more private companies and venture-backed startups. We also noted that many of the most practical near-term benefits of space were likely to show up on Earth first: better GPS, improved logistics, global transparency, disaster response, broadband access, artificial intelligence, and advanced manufacturing.

At the time we were directionally right, but the framing has shifted. Lower launch costs make space more accessible. The next question is what lower launch costs make possible. The rocket is not the entire thesis, just the entry point.

That is what made the Space Walk III startup mix so interesting. The companies did not appear to be chasing the visual drama of space. They were working on the less glamorous layers that make a functioning space economy possible over the long term.

The pending SpaceX IPO may accelerate this conversation. Public attention will likely focus on valuation, Starship, Starlink, and Mars. SpaceX is the company most responsible for changing how investors, customers, and governments think about the commercial space industry. Travel to space, the Moon and Mars is becoming more about the demand signal for energy, logistics, construction, life support, and autonomy.

Railroads provide a similar historical comparison. The headlines were often about the trains themselves, but the railroads created demand for much broader infrastructure: standardized time zones, coast-to-coast telegraph communication, large-scale freight logistics, and new patterns of land development. The trains were the rockets of the past.

Space may follow a similar path. The first wave is access. The second wave is infrastructure. The third wave is applications.

From a venture capital perspective, the most interesting companies may not be pure space companies. They may be companies solving hard problems for extreme environments, where space is the forcing function and Earth is the first market. A power system designed for space may also support remote industrial sites, defense installations, offshore energy operations, or disaster recovery. A water recycling system designed for a lunar base may have applications in agriculture, mining, military deployments, or water-stressed regions. A robotic construction system designed for the Moon may be useful in hazardous industrial environments on Earth. A communications system built for space may improve aviation, maritime, emergency response, and rural connectivity.

That is where the venture opportunity becomes more compelling. The best space-related companies may not need space revenue on day one. They may be building products for terrestrial customers while preserving long-term optionality as the space economy matures. Space can increase the scale of the opportunity, but Earth may still provide the first customers, initial revenue, and proof points. Space just becomes the most challenging version of the problem.

Inflection Points

Launch as an access layer. Declining launch costs make space more accessible, but the larger opportunity may come from infrastructure that becomes viable as access improves.

Infrastructure becomes the focus. The next phase of space investing may focus more on logistics, power, construction, communications, life support, biotech, and autonomous operations.

Earth-first commercialization. Many of the most attractive space-related startups may sell into terrestrial markets first, including defense, energy, industrials, agriculture, telecom, healthcare, and disaster response.

Space as a moat. Operating in extreme conditions becomes the moat for innovation in reliability, autonomy, resource efficiency, and closed-loop systems.

Rockets will always capture attention. They are the dramatic and visible symbol of space. But the next wave of venture opportunity may belong to the companies making space useful.

Thanks for reading,

-Eric.