FTX Review

Evaluating the FTX saga from an investment perspective

Happy Thursday, 👋

Most of us have seen the news regarding the FTX implosion, a company which received almost $2 billion in investments from over 80 well known funds. The FTX downfall remains a debate between fraud, poor management, or a combination of both. Regardless of the outcome, looking back at failed investments is helpful for becoming a better investor, founder, advisor, or team member.

A Recap

The public downfall of FTX started November 2nd when CoinDesk published a partial balance sheet for Alameda, the FTX trading division. Despite showing assets of almost $15 billion, a majority of the assets were Alameda tokens developed by FTX. Tokens are similar to owning stock in a company, so essentially Alameda’s balance sheet showed a significant portion of its assets were a private stake in FTX.

The concentration of assets in an illiquid position all under the same corporate structure led Binance, a large third party holder of FTX tokens, to become concerned and start selling its position. As Binance sold, the value of the FTX tokens dropped by almost 40%. On November 8th Binance made a non-binding offer to acquire all of FTX. After two days of due diligence, Binance walked away citing too many concerns with FTX. Within 48 hours FTX filed for bankruptcy.

Enron Parallels?

Years ago another company named Enron made markets in illiquid and unique financial instruments ranging from electricity to broadband. John J Ray III was appointed to lead the Enron bankruptcy process and now 21 years later he is doing the same for FTX.

Along with bankruptcy leadership from John J Ray III, there are several other parallels between Enron and FTX.

Enron issued debt collateralized by its stock price. Enron’s stock was originally viewed as a strong blue-chip name with little risk of default, but as Enron’s stock price declined, its balance sheet quickly evaporated. Alameda faced a similar demise as the decline in value of the FTX token on its balance sheet quickly brought down the combined entities.

Dynegy, one of Enron’s competitors made a non-binding acquisition offer after Enron’s value started to decline. Binance made a similar offer to FTX only days after its troubles started. Ultimately Dynegy walked away from the Enron deal after finding too many conflicting diligence items, similar to how Binance decided against purchasing FTX.

Four days after Dynegy walked away, Enron filed for bankruptcy. FTX was a bit faster as it took only two days to declare bankruptcy after Binance pulled its acquisition offer.

The bankruptcy filings of both Enron and FTX indicate lax internal controls, uncertainty with financial statements, and general mismanagement resulting from exponential growth.

Poor Management or Fraud

The FTX debate will take time to decide if there was fraud, mismanagement, lack of experience, or some combination. Only a few months ago FTX raised $500 million from several prominent investors at a $32 billion valuation, making its downfall even more surprising. Reviewing details from the bankruptcy will help all investors better evaluate their own diligence process as it reinforces the importance of sticking to fundamentals even if it means missing out on a deal.

From the Bankruptcy Pleadings per John J Ray III: Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here. From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented

Poor Management or Fraud —> Poor Management?

Several bankruptcy disclosures indicate a lack of management experience at FTX. The exponential growth may have been too fast for the inexperienced executive team. It is not uncommon for new founders to spend more time focusing on building the product and less time on managing the business, which is often where early stage venture investors or board members can step in and offer guidance.

🏢 The absence of corporate governance at FTX indicates a lack of experience building a company but also suggests investors may have been less active from a board or advisory perspective.

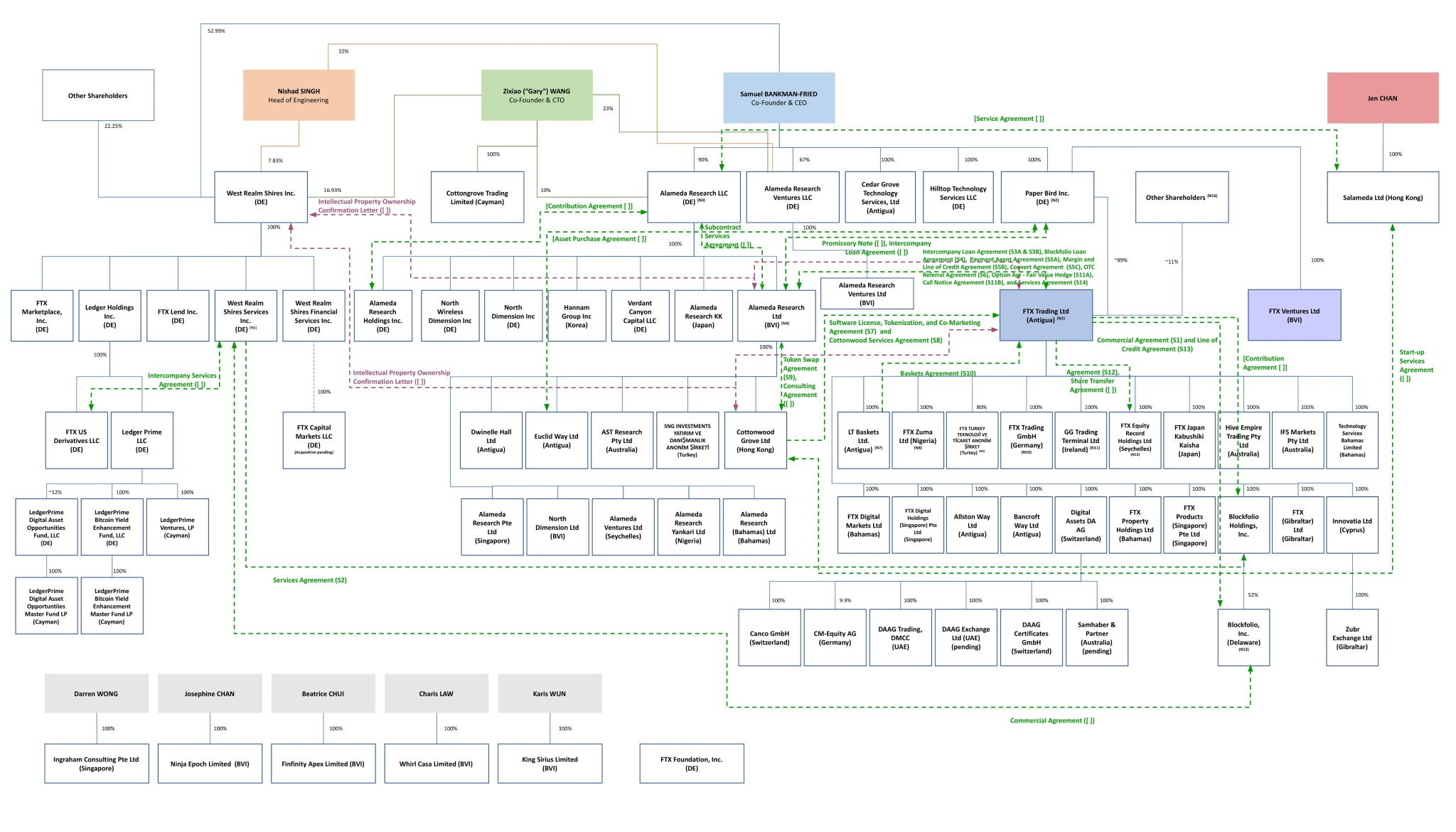

Bankruptcy Disclosures: Many of the companies in the FTX Group, especially those organized in Antigua and the Bahamas, did not have appropriate corporate governance. I [John J Ray III] understand that many entities, for example, never had board meetings

👨👩👧👦 The employee base increased so quickly the company lacked even a basic human resources department. Without a structure for team resources it becomes difficult to build a corporate culture, maintain corporate security, and provide employee development opportunities.

Bankruptcy Disclosures: Debtors have been unable to prepare a complete list of who worked for the FTX Group as of the Petition Date, or the terms of their employment.

💳 Culture is often set by how employees perceive basic company policies such as expense reimbursements. A culture where policies are lacking or not well defined is often the result of inexperienced management teams not realizing a need to define internal structures.

Bankruptcy Disclosures: The Debtors did not have the type of disbursement controls that I [John J Ray III] believe are appropriate for a business enterprise. For example, employees of the FTX Group submitted payment requests through an on-line ‘chat’ platform where a disparate group of supervisors approved disbursements by responding with personalized emojis.

Poor Management or Fraud —> Fraud?

To date the FTX disclosures have not indicated substantial fraud, although initial bankruptcy disclosures suggest more details may be uncovered as the layers are pealed back on internal operations.

🏠 Use of company assets for personal purchases requires significant disclosure and reporting. The lack of general corporate governance at FTX may not be a great excuse for the misuse of investor money.

Bankruptcy Disclosures: [C]orporate funds of the FTX Group were used to purchase homes and other personal items for employees and advisors. I [John J Ray III] understand that there does not appear to be documentation for certain of these transactions as loans, and that certain real estate was recorded in the personal name of these employees and advisors

🔑 Many of the FTX disclosures suggest mismanagement, but the company was built by highly technical people which makes us wonder why they would not use better communication protocols.

Bankruptcy Disclosures: Unacceptable management practices including the use of unsecured group email account as the root user to access confidential private keys and critically sensitive data for the FTX Group companies

🔐 Some levels of communication used unsecured email accounts for highly confidential communications while other communications were routed through programs using advanced techniques to hide all discussions.

Bankruptcy Disclosures: Unacceptable management practices included…use of software to conceal the misuse of customer funds.

One of the most pervasive failures of the FTX.com business in particular is the absence of lasting records of decision-making. Mr. Bankman-Fried often communicated by using applications that were set to auto-delete after a short period of time, and encouraged employees to do the same.

Were Investors Part of The Problem?

Over 80 investors funded FTX, which may have reinforced the actions of the management team. Venture capital funds invested almost $2 billion into the company which may have conveyed a level of support and approval for the company’s existing way of doing business.

It’s surprising we have not heard about FTX investors pushing for stronger corporate governance practices. Even a basic procedure for tracking cash within the company was missing, indicating either investors were misled about corporate operations or investors feared missing out on a chance to invest so disregarded basic diligence.

Bankruptcy Disclosures: The FTX Group did not maintain centralized control of its cash. Cash management procedural failures included the absence of an accurate list of bank accounts and account signatories, as well as insufficient attention to the creditworthiness of banking partners around the world.

Because of historical cash management failures, the Debtors do not yet know the exact amount of cash that the FTX Group held as of the Petition Date.

What About the Auditors?

FTX did have audited financials, although the process raises a few questions. The international operations of FTX were audited by Prager Metis, a US firm with annual revenue of $140 million. The US business was audited by Armanino, a slightly larger firm with $460 million in revenue but still small compared with the average Big Four (Deloitte, PwC, E&Y, KPMG) revenue of $40 billion.

Small audit firms such as Prager or Armanino often have great people working for them, but we wonder why investors would not have requested a larger audit firm handle the engagement. A concern with relying on smaller audit firms is the percentage of revenue generated from a single client, especially one as large and complex as FTX. Not implying wrongdoing by the auditors but when one client becomes a significant portion of audit revenue we start to get nervous about independence.

Even the bankruptcy CEO John J Ray III expressed concern in one of his statements, indicating “I have substantial concerns as to the information presented in these audited financial statements.” The bankruptcy filings list over 100 entities, which is a sizable corporate structure for even the largest audit firms to understand

Wrapping Up Our Discussion

Studying company successes and failures is one of the best ways for investors, founders, executives, and team members to improve. The FTX saga has gained a lot of attention due to its size and number of prominent investors, but the lessons apply to companies of any size. The debate over fraud or mismanagement may never be resolved but evaluating the growth and decline of FTX demonstrates why corporate policies, controls, governance, and independent boards are an important component of any company.

Venture capitalists are often the first outside group to dig into the inner workings of a company, which is why they often need to become advisors along with being investors. The FTX downfall reminds us of the challenges involved with venture investing as even the most recognized investment firms can make mistakes. Protecting the downside for venture capital investments starts with asking the hard questions, making sure the corporate structure is solid and the right procedures are in place. Due diligence may not be the most exciting part of venture investing but done right it helps identify reasons to pass on a deal when everyone else is moving forward.

Thank you to all our new readers as our newsletter family continues to grow. If you know someone who might be interested in our discussions, let them know about us as we always enjoy having more smart readers join us every few weeks.

Wishing everyone a great weekend.

-The Caymont Team.